Grants and loans share one big advantage over taking on investors: both are non-dilutive. You get the money without giving up a slice of your company. That alone puts them ahead of equity for a lot of founders. But the similarity stops there. One you keep, the other you pay back, and the situations where each makes sense are almost opposite. Here is how to tell them apart, what each actually costs you, and why the smartest move is often to use both.

The one difference that matters most

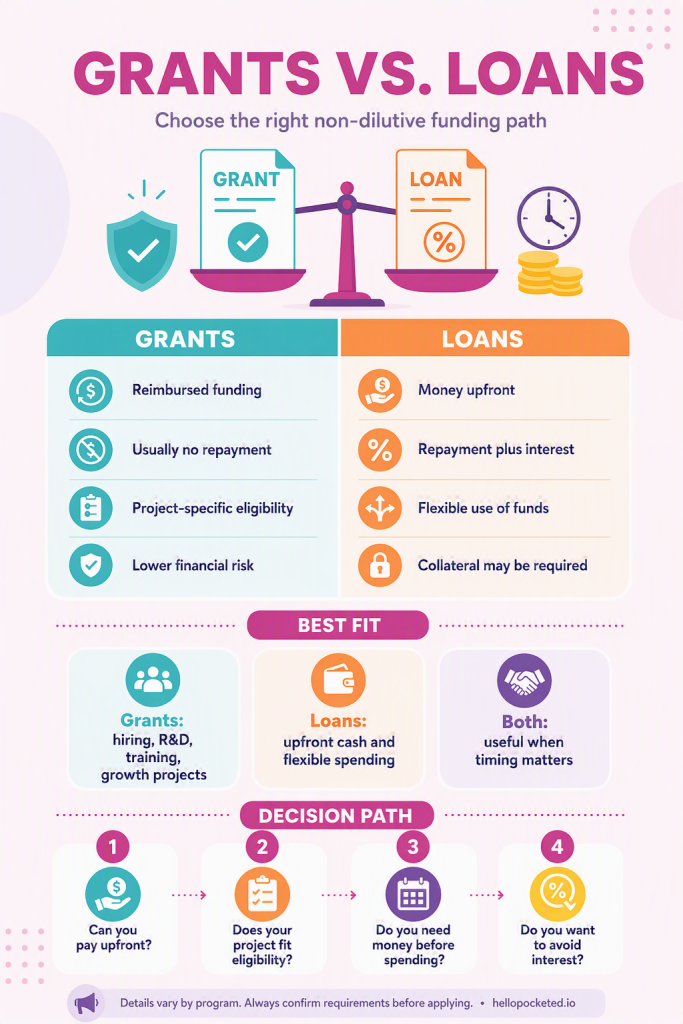

Everything else flows from this: a grant is money you keep, and a loan is money you rent.

When you win a grant, you do not pay it back, as long as you follow the program’s rules. It is not quite “free,” since you still invest the time to apply and usually have to cover part of the project cost yourself, but no repayment ever comes due. A loan is the reverse. You get the money now and pay it back later with interest, so you will return more than you borrowed. Useful, but it is debt.

That single distinction drives everything else, including the trade-offs below.

Where grants win, and where loans win

Each is better at almost exactly what the other is worse at.

Grants win on cost. They are the cheapest capital you will ever find, because you keep the money and your equity. The catch is everything around the money. Grants are competitive, so you might apply and not win. They open on their own schedules rather than on demand. They restrict what you can spend on. And many reimburse you only after you have spent, which means you need cash on hand to front the project first. Eligibility hangs on your project and your profile, not your finances.

Loans win on speed, certainty, and flexibility. The money arrives up front, often fast. BDC can fund a small business loan in under a week. You can usually spend it on almost anything the business needs, the amount is sized to what you can repay rather than to a contest, and lenders are open year-round. The price is the interest and the fact that it sits on your balance sheet as debt. Approval depends on your creditworthiness, your revenue, and sometimes collateral, rather than on a project’s merit.

Put simply: a grant costs you effort and patience, a loan costs you interest and certainty of repayment.

A quick word on collateral

This is one place loans get riskier. Grants almost never ask for collateral. Loans often do, meaning an asset like property or equipment that the lender can seize if you fail to repay. If a bank lends you $100,000 and your business cannot pay it back, that collateral is how they recover their money.

Government-backed options soften this. The Canada Small Business Financing Program has the federal government cover 85% of a lender’s loss on a default, which makes banks far more willing to approve businesses with limited collateral, for loans up to $1.15 million. BDC, Canada’s bank for entrepreneurs, and Futurpreneur, which lends up to $75,000 plus two years of mentorship to founders under 40, are both built for earlier-stage businesses that a traditional bank might turn away.

The blurry middle

Grants and loans are the two ends, but plenty of funding sits in between, and knowing it exists saves confusion.

A repayable contribution is government money for a specific project that you pay back, sometimes only if the project succeeds. A forgivable loan is a loan that converts into money you keep if you hit agreed conditions, such as creating a set number of jobs. Both blur the line on purpose. When you are comparing options, the question is never just “grant or loan,” it is “how much of this do I keep, and under what conditions.” Our grant glossary breaks down each of these terms if you want the precise definitions.

Grants and loans are the two ends, but plenty of funding sits in between, and knowing it exists saves confusion.

A repayable contribution is government money for a specific project that you pay back, sometimes only if the project succeeds. A forgivable loan is a loan that converts into money you keep if you hit agreed conditions, such as creating a set number of jobs. Both blur the line on purpose. When you are comparing options, the question is never just “grant or loan,” it is “how much of this do I keep, and under what conditions.” Our grant glossary breaks down each of these terms if you want the precise definitions.

You do not have to choose

Here is the part the “grant or loan” framing misses entirely: the two work beautifully together.

Because most grants reimburse you after you spend, a short-term loan or line of credit can bridge the gap. You borrow to fund the project now, then pay the loan down when the grant reimbursement lands. That solves the single biggest practical hurdle with grants, which is needing cash up front to access money you have already been approved for.

The relationship runs the other way too. Every grant dollar is a dollar you do not have to borrow or give away. Win a grant that covers 50% of a project and you have just halved the loan you need, along with the interest on it. Use grants to shrink the debt, and use the debt to make the grants usable.

So where should you start?

For most businesses, start with grants. They are free, they are non-dilutive, and you may find you do not need to borrow as much as you thought, or at all. Then reach for a loan to cover what grants will not fund, to move faster than a granting cycle allows, or to bridge the wait for reimbursement.

You are the one steering the business, so the right mix is yours to choose. The point is that it is a mix, not a single pick.

Not sure which grants you qualify for in the first place? That is where Pocketed’s platform comes in, surfacing the non-dilutive funding your business is eligible for so you can borrow less and keep more. For a head start, see our 3 Easy Grants to Apply for in 2026.